AUTHORS

Roberto Ferrari

Partner Digital Financial

Services

Roberto Nappi

Senior Manager – Banks

and Payment Systems

Andrea Taglioni

Director @Bip xTech

The advent of Open Banking undoubtedly represents one of the most significant changes in the world of financial services. The core of this potential revolution is, first and foremost, the change in perspective with respect to financial data and its actual ownership, which becomes, thanks to PSD2, the sole responsibility of the customer. It’s a power shift, against the traditional asymmetry of information between bank and client, all in favor of the client and, ultimately, those who will best serve him.

The basic principle of Open Banking is not just about opening up to non-bank competitors. In fact, it consists primarily in the unrestricted use by customers of information on their personal financial transactions. Something that should be normal, implicit, but has never been so.

The complete control over this information is also combined, for the client, with an overall expansion of choice, thanks to the sharing of data with third parties able to provide new financial services in a way that is innovative compared to the traditional bank. This is the second focal point of Open Banking: the increase in competition in the supply of financial services due to the possibility of sharing users’ financial data with third parties, including non-banks.

Increased competition, as usual, will produce over time an enhanced offering for the end customer, but potentially also a dramatic change in the competitive landscape in 5-10 years.

To simplify, what could happen to the banking world is similar to what has happened in the recent past to mobile phone operators with respect to digital messaging services such as Whatsapp, Messenger, Wechat, etc. What the banking world may risk, in fact, is that this improved offering will be more effectively carried out by third parties, digital TPPs (Third Party Providers), who are more receptive and prepared with respect to the models and technologies needed to leverage customers’ transactional and financial data and information.Banks that are not responsive, in essence, are at risk not only of being left behind, should they fail to innovate their own models by taking advantage of Open Banking, but also of finding themselves facing very fierce competition, not only from FinTech startups but also from leading companies in other sectors all the way to the global Big Techs.

The race will be towards a new model of digital unbundling and rebundling, where many different players will be able to position themselves as financial services platforms, or open hubs capable of aggregating, in an efficient and customer-friendly manner, a large number of products and services also developed by other financial and non-financial companies.

Everyone will have to find their own new optimal digital configuration, starting from their assets and evolving their business models. Banks themselves will be able to increase their competitiveness if they can use a more proactive approach.

The challenge will be in gaining and at the same time maintaining control of customer relationship. Who will be the client’s entry point to the newly defined financial services? Will there be several of them? Will unresponsive banks risk being confined to managing the back-end backbone to ensure smooth transactional flows, like mobile operators for phone and data traffic, and little else?

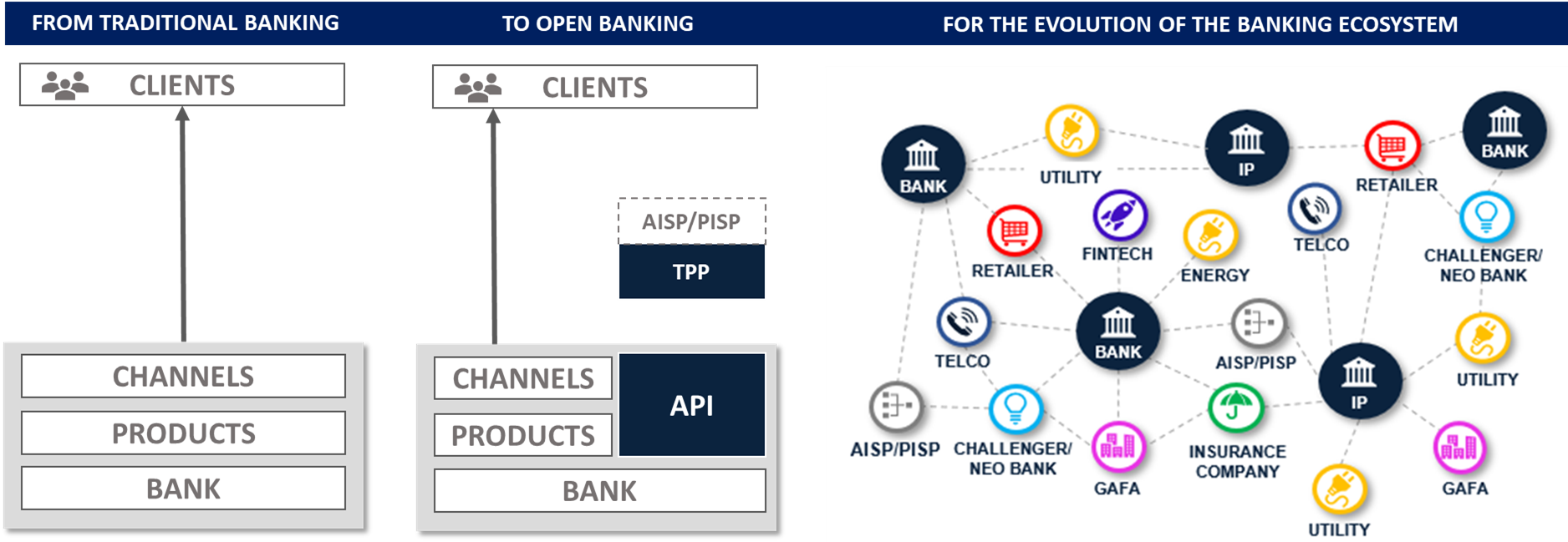

From PSD2, Beyond PSD2

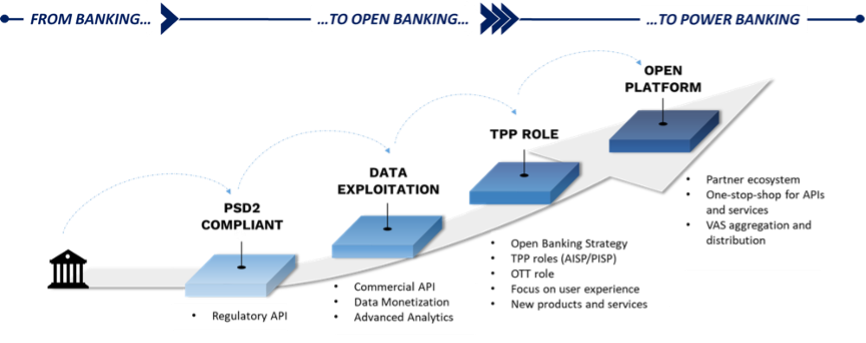

On European soil, the advent of Open Banking overlaps with the entry into force of the now well-known PSD2, in 2018, which is driving Europe to be a testing ground and vanguard of the new competition models in the sector (along with Great Britain and Australia, which started around the same time). This has happened first because of the mandatory access to accounts by third parties enshrined in it, whose technological prerequisite is the opening of banking APIs relating to the transactions of customers’ current accounts. It is precisely PSD2 that has therefore regulated the full availability of one’ s own data by the banking customer, at the same time making it easier for the most innovative financial and non-financial companies to offer different and innovative services, giving consumers more choice. In the UK, the implementation of the Open Banking regulation started about 12 months ahead of PSD2 in Europe, so it is already possible to see what has occurred. The usage of typical PSD2 activities and services, such as account aggregation and third-party account payments, has increased significantly after an initial settling-in period of around 9 months. This usage, as quantified by the number of API calls, grew from just under 67 million calls in 2018 to about 1 billion in 2019, reaching nearly 6 billion in 2020, effectively multiplying by ninety times in just two years.

The expansion of the offer has undoubtedly involved the banking world, which in some cases has begun to take advantage of the opportunities implicit in the regulations, initially by developing account aggregation solutions and services with the aim of maintaining its pivotal role in the relationship with its clients, in order to counter similar offer proposed by fintech startups and Neobanks/challenger banks.

Secondly, we are beginning to witness, at various levels and still in a disorganized fashion, the emergence of more evolved solutions and competitive behaviors, with the launch of new use cases and services built on data, in the lending and in the saving and wealth management worlds, up to the exposure of commercial APIs for data monetization and Advanced Analytics solutions and services, and finally the creation of the first Open Banking ecosystems.

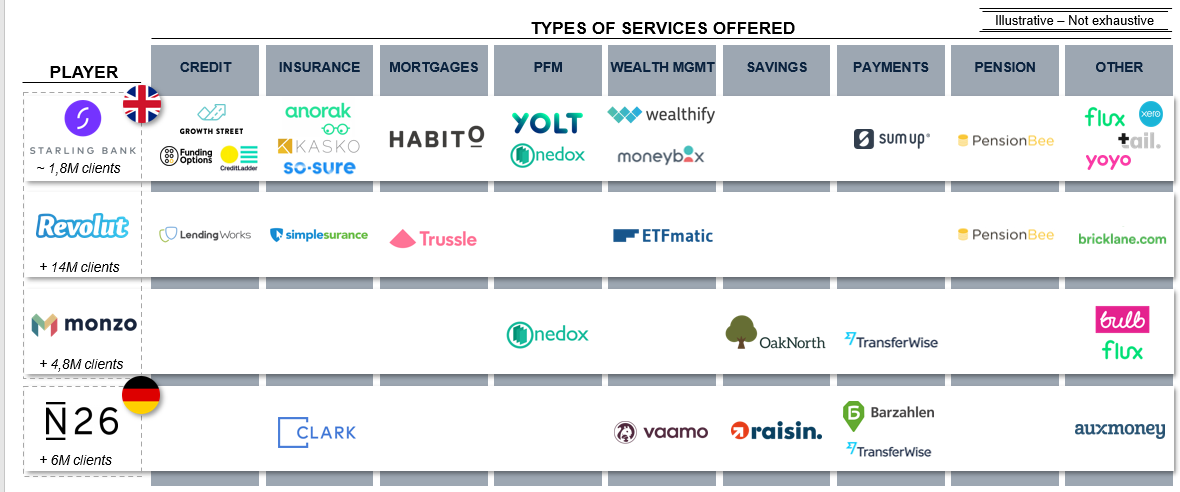

As previously mentioned, however, we can see how new players are beginning to enter the sector, being capable of exploiting the opportunities produced by the new regulations, making the best use of digital technologies. Fintech, Big Tech, and service companies such as utilities and Telcos are beginning to compete with traditional banks, offering financial and/or payment services with digital architectures and solutions, therefore far more agile, fast and customer centric. Very often, in this initial period of implementation of Open Banking regulations, banks have approached PSD2 requirements as a pure compliance issue, leaving room for new competition. The entry in the market of these new companies is beginning to soften and blur the boundaries of the banking sector, creating a mixture of banks and third parties in a new, open competitive landscape. In this scenario, challenger banks (or Neobanks) are perhaps the epitome of the wave of innovation brought forth by Open Banking. These are next-generation digital banks, focused on, but not limited to, a younger audience, founded with the specific intention of capturing the digital revolution and leveraging the benefits of openness and data sharing, while serving as a platform that can aggregate vertical fintech services. The exponential growth of the number of users of these next-gen digital banks represents a clear message that traditional banks must take note of. Starling Bank, the “most open” neobank on the market, already has 1.8 million customers in the UK, to whom it offers the services of at least 15 other FinTech startups, perfectly integrated on its platform. Furthermore, Revolut and N26, the two European Neobanks with the largest number of customers, serve 14 and 6 million users respectively, and have fully embraced the new Open Banking paradigm, also aggregating many third party fintech services within their offerings.

The key breakthrough for banks: Power Banking

The increase in competition, the revolution in service models, the arrival of new players in the market and the margin squeezes on some segments of the value chain are certainly not an insurmountable obstacle, especially for those banks that have decided to adapt their way of doing business to this new phase. Traditional banks can still count on a number of key assets that challenger banks, for example, are struggling to replicate: the wide user base, the regulatory know-how, the brand, the in-depth know-how of the full range of banking products are still a difficult gap to bridge, especially for digital banks that, in the early stages of their development, are focusing on an offer consisting of cheap, fast and low-margin services. Challenger banks offer ease of use, fast onboarding and a high-level UX for many simple products such as current accounts and debit cards, but not many have managed to replicate these features for more structured and complex products, necessary to make a profit in the banking business.

Traditional banks must therefore leverage on these strengths and at the same time embrace the innovative push of new market entrants, in order to offer a new UX, combined with a more adaptive personalized and contextualized offer, aligned with the digital experience proposed by the new players. The key to capturing this innovation is not so much the technology (there are now many suitable technology providers), but the adoption of a new mindset, a new understanding of their role in the financial ecosystem, which will evolve their business models and go beyond the vision of compliance-driven digitization, or of a digital transposition of pre-existing physical structures and processes. New technologies can now be bought, without the necessity to develop everything in-house, and this opens up important opportunities for banks themselves.

The solution is to move towards Power Banking, i.e. positioning the bank, backed by its assets, as a hub at the center of an ecosystem of partnerships, which aggregates and distributes high value-added financial services also provided by third parties, channelling them through a one-stop-shop of APIs and services. This is the way to embrace the Open logic: from providing traditional services to becoming primarily platforms for the provision of services, incorporating the offerings of FinTech and other players, which are becoming increasingly numerous and varied.

It takes vision, adaptability and expertise to implement a strategy that works in this direction and enables Power Banking as we have described it. The underlying element of this strategy is the enhancement of the banking data, through a high capacity of real time or near real time availability, analysis and processing. The central element of Power Banking is therefore data, and it is no coincidence that it is precisely the element that we have highlighted as the cornerstone of the Open Banking revolution, which is itself evolving towards Open Finance, with a wide range of players and competitive offers.

Beware that, if the availability of a large customer base and the expertise to use data become key elements of the new digital evolution of financial services, Big Tech and Big Players from other industries (from Energy to Telco to Logistics/e-Commerce to Postal Services) can also come into play. They have, in fact, already begun to do so, with the aim of finding synergies of service, new sources of revenue, and better customer knowledge. Hybrid services will appear across banking, insurance, telephone companies, retailers, logistics and transport.

We are facing a new competitive scenario, with different business models, even very different from the traditional universal bank model, that can exploit new opportunities to the benefit of users in terms of opportunities and service levels.

As previously stated, the key enabler of this new ecosystem will definitely be data.

These last five years have seen the explosion of Artificial Intelligence (AI) and Cloud solutions, which now offer an extraordinary support to leverage information to create new value-added services.

The data flow at the Open Banking network is in itself an enabler that will “democratize information” among all players, but those who know how to use AI to “invent” something new will gain a huge competitive advantage.

Thanks to AI it will be possible to investigate the spending behaviors of users, understanding their inclinations, habits, needs: many banks already analyze transactions through AI algorithms to define their marketing strategy, enabling upselling (“do you want to increase the card limit?”) and cross-selling (“you have the account, why don’t you apply for a mortgage?”) proposals.

The complexity of these algorithms is increasing, as they analyze life events in relation to expenses (birth of a child, marriage), or examining relationships between individuals by defining real networks of interaction. At last, the banking offer can be personalized.

With Open Finance this power will be amplified: we will see the emergence of hyper-specialized players on vertical algorithms, as whoever offers the best appetite scoring algorithm for a micro-loan will be able to sell it to others, or to players in other industries. External data will be used extensively, combining transactional and banking data with info-provider data or, within the limits of privacy regulations and with appropriate consent, other web/social sources. Above all, we will see players from other sectors use their enormous data assets to “merge” them with those of banks in order to obtain synergies: think of Telcos that can know the mobility of every individual through cell tower data, or OTTs that know customer behaviors and social networks, or e-commerce players that know their propensity to purchase common goods. The financial services experience will become increasingly contextualized.

AI as a data trigger engine is an unstoppable trend and, combined with the arrival of 5G (mobile TLC technology that enables the creation of “connected ecosystems of objects”), will lead to the “real-time” experiences in all classes of service: we will receive interactions, proposals and/or customizations while we are making transactions or immediately after. In this way, it will also be possible to trigger competitive mechanisms between Payment Service Providers and Banks about instant payment services.

All this will also be possible thanks to the advent of the Cloud in the banking world. Hindered for years to “hold” the information assets within the bank boundaries, today the Cloud has been legitimized, thanks to PSD2, Open Banking and generally to a greater flexibility of the banking regulator.

The data flow required by these regulations renders useless the anachronistic defensiveness held until just recently: some banks have started the process of massive transition to the Cloud, which will take place in the next two years.

Cloud means infinite computing power, speed of information access from any point of the network, lowered entry barriers to create any service (no need to buy expensive servers) and scalability (with well-designed architecture it will be possible to go from a few to millions of users without particular problems). AI and Cloud today go hand in hand: all Cloud providers include AI tools by design and ready-made APIs for basic services like chatbot, text and image recognition, etc.

With a good idea, with the right data, and starting with minimal infrastructure costs thanks to the cloud, it will be possible to create the future Netflix of banking: this will inevitably drive innovation throughout the industry at the expense of those who fail to innovate.

Power Banking and Power Finance, the next appointment

In this article we have always discussed Open and Power Banking but, as mentioned several times throughout the paper, the subjects involved are much more numerous and varied than just banks. The scenario we have described is well suited to encompass numerous business sectors, which can make use of the opportunities offered by the opening of bank data in the wider perspective of Power “Finance”, becoming an active part of the banking ecosystem and increasing the offer to their customers. The same traditional banking players, the incumbents, can turn the situation in their favor by reactively exploiting the emerging opportunities. The scope of the possibilities created and how these strategies can be implemented will therefore be the subject of a subsequent article.

The Bip “Open Banking & Finance” and “xTech” Centres of Excellence, support many customers in financial and non-financial world leveraging on our skills in Banking, Payments and Fintech and Data/AI/Cloud/Blockchain/5G in order to exploit Open Banking by optimizing, enriching and evolving their business through new innovative services.

Bip Centres of Excellence have a worldwide coverage: as an example we are supporting, through our Advisory Services, the Brazilian Banks Association (ABBC) in the set-up of Open Banking in Brazil.

If you are interested in learning more about our offer or would like to have a conversation with one of our experts, please send an email to [email protected] with “Open Banking” as subject, and you will be contacted promptly.

Read more insights